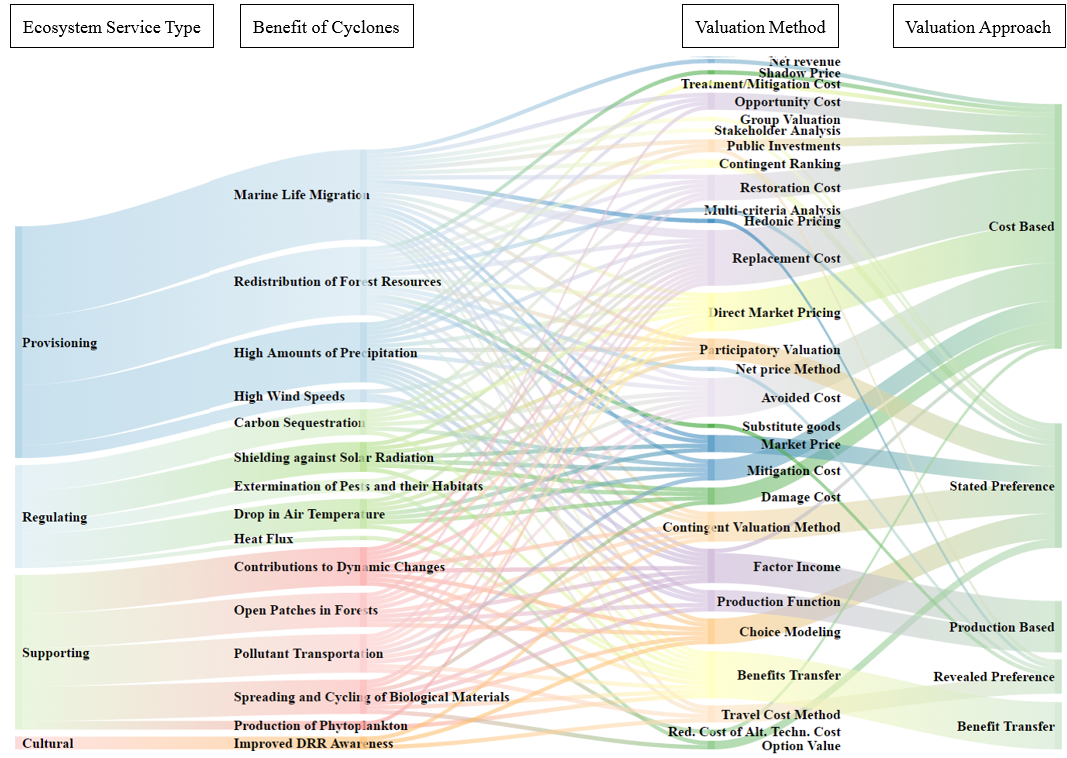

The final step in this study was linking the benefits of cyclones as ecosystem services to known monetary valuation methods.

The benefits of cyclones and their corresponding ecosystem service types were linked to two sources containing valuation methods: 1) the conceptual matrix and example methods of ecosystem service valuation from Pascual & Muradian (2010), and 2) the near 1500 valuation methods from studies in The Economics of Ecosystems and Biodiversity (TEEB) database (Van der Ploeg & De Groot, 2010). In these sources, the valuation methods corresponding to cyclone benefits were categorized into five different approaches: cost based, stated preference, production based, revealed preference, and benefit transfer. All identified benefits were considered from the perspective of benefit to humans in order to be valued, including certain benefits from literature that were not directly classified as beneficial to humans. In these systems, these five valuation approaches are described as follows:

• Cost based approaches depend on the estimation of the costs of recreating the service by artificial means.

• Stated preference approaches apply surveys about a market with demand for services and hypothetical policy changes in the availability of these services.

• Production based approaches estimate how much services improve resources or environmental qualities, lead to lower costs and prices of marketed goods, and thus enhance income or productivity.

• Revealed preference approaches are based on observing individual choices in existing markets and services that are related to the services requiring valuation.

• Benefit transfer approaches rely on the outcomes of a previous valuation from an area with a comparable ecosystem to the study area. If these two are comparable, the value can be transferred, or certain adjustments to reflect local circumstances can be applied.

The final results (see figure) show that the applied valuation methods for comparable services were mostly related to the identified provisioning services, and most of the valuation methods used were cost based, namely replacement costs, direct market pricing, and avoided costs.

No comments:

Post a Comment